The JSE has shone the spotlight on the small-caps sector with a webcast featuring some of the hot shares in this sector.

CEOs and senior executives from Afrimat, Stadio Holdings, Balwin Properties, Trellidor, Master Drilling and Trematon Capital Investments shed light on their business fundamentals, their plans for expansion, and investment opportunities.

Small caps often outperform large caps as they offer higher growth prospects and, from a valuation perspective, they trade at a lower price-to-earnings multiple.

An added benefit of small caps is easy access to their management, so watch the clips below to hear how these companies see the road ahead.

PICTURE: MICHAEL ETTERSHANK

Read More

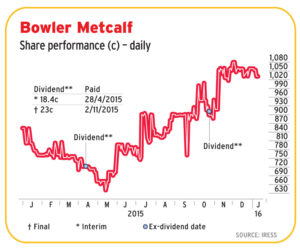

Bowler Metcalf. This plastics packaging specialist initially spooked the market when it walked away from a major client when the pricing levels were no longer viable. It has since found an abundance of new business at acceptable margins, and appears to be making its investment in technology pay off handsomely. The share is fundamentally cheap, and there could be a medium-term bonus when it lists its soft-drink investment, SoftBev.

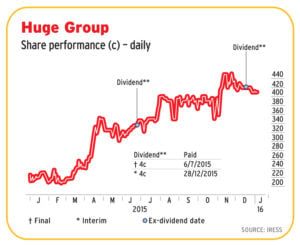

Bowler Metcalf. This plastics packaging specialist initially spooked the market when it walked away from a major client when the pricing levels were no longer viable. It has since found an abundance of new business at acceptable margins, and appears to be making its investment in technology pay off handsomely. The share is fundamentally cheap, and there could be a medium-term bonus when it lists its soft-drink investment, SoftBev. Huge Group. This is a gut-feel call. Operationally things have started to ring for this small telecoms specialist, but we suspect there might be a good chance of value unlocking via corporate action.

Huge Group. This is a gut-feel call. Operationally things have started to ring for this small telecoms specialist, but we suspect there might be a good chance of value unlocking via corporate action. Prescient. This asset manager has not caught the market’s fancy in spite of the rush to back newer listings in the sector. But Prescient’s low equity model might be an advantage in jittery market conditions in the year ahead. Did we mention that CEO Herman Steyn does not draw a salary, but opted for remuneration in the form of a scrip holding?

Prescient. This asset manager has not caught the market’s fancy in spite of the rush to back newer listings in the sector. But Prescient’s low equity model might be an advantage in jittery market conditions in the year ahead. Did we mention that CEO Herman Steyn does not draw a salary, but opted for remuneration in the form of a scrip holding?